All Categories

Featured

Table of Contents

Because of this, lots of people pick the irreversible alternative, guaranteeing that their household will have the money required to pay their end-of-life expenses. If your last cost policy expires, you will certainly not be able to restore the exact same plan, however you can purchase new coverage. The disadvantage of this is that your new policy will likely set you back even more, since rates for brand-new policies increase based on exactly how old you are.

All life insurance policy plans give a death advantage, or payment when the policyholder is no much longer living. This money will after that go towards the policyholder's desired costs and recipients. Generally, final expense survivor benefit range anywhere from $5,000 to $50,000. There are essentially no limitations a strategy can impose on what you can put this cash in the direction of.

Fidelity Funeral Insurance

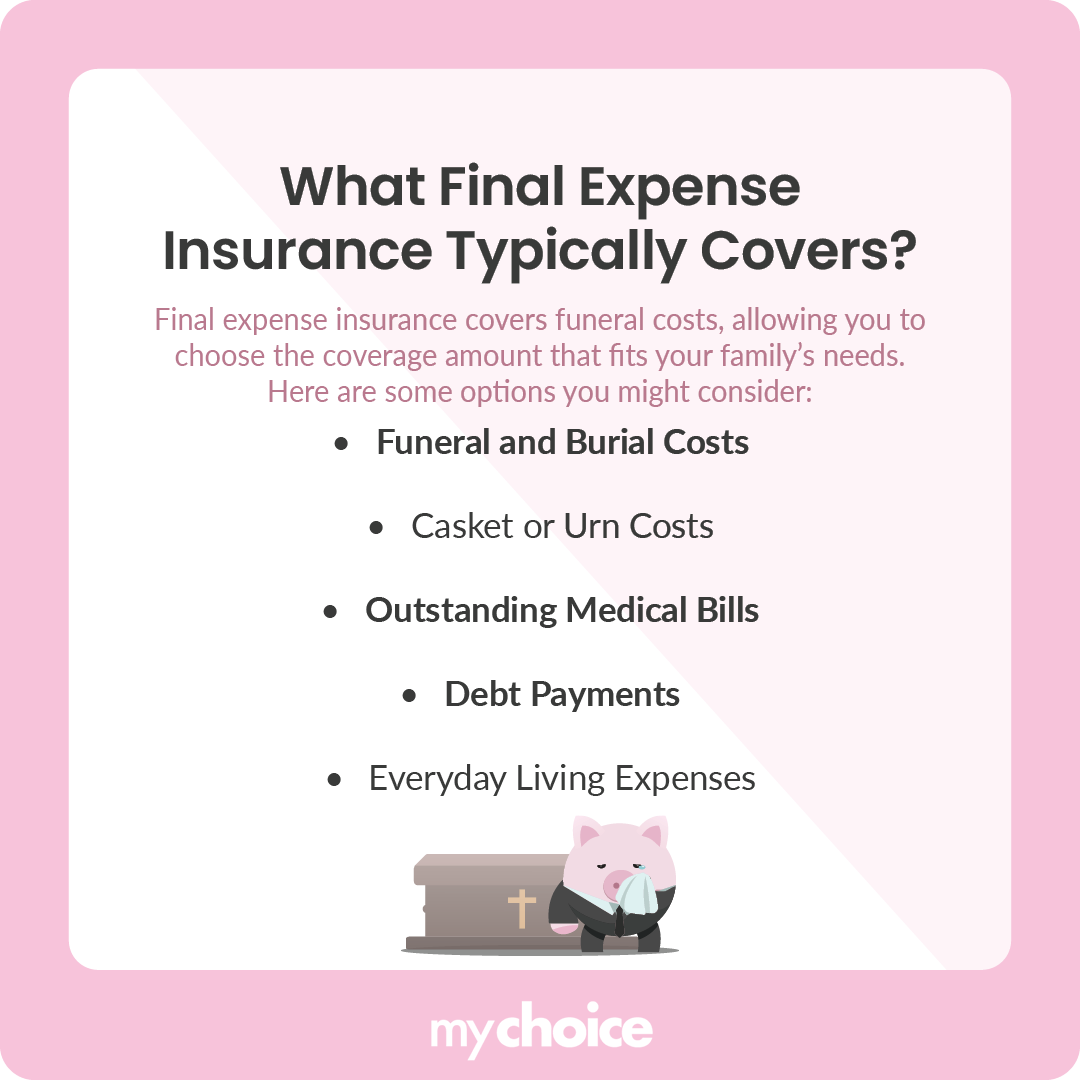

These can possibly consist of: Funeral ExpensesMedical BillsFinancial Assistance for Liked OnesPersonal LoansInheritanceBusiness Companion SharesEstate Taxes, and More Nevertheless, for all of these potential uses, you should divide your payout of $5,000-$50,000 to each of them. You need to pick what and how much to add in the direction of it. While it wasn't provided above, living costs are an additional prospective use of the last expenditure payment.

You can definitely set apart funds for this purpose, however it may be exceptionally restricted based on just how much they require and what else you intend to use it for. Say, for example, you desire to use it for your funeral expenditures and your liked one's living expenditures. If the typical funeral expenses around $6,000, you'll need a payment that's more than $6,000.

You'll require at least a $12,000 death benefit, and even more if you desire to use it for other things. You can additionally use your final expenditure policy for your very own living costs. This might be high-risk. As soon as you begin using the survivor benefit, your monthly payments will not transform, and the payment will not boost, just decline.

Does Life Insurance Pay For Funeral Costs

Term life plans are a bit bigger and less complicated to utilize for this objective. Term life, however, is extra challenging to certify for than last expense. And, this doesn't suggest that last expense is an even worse optionit's still unbelievably helpful. Donating your body to scientific research is a vital decision. Those that choose to contribute their body to scientific research might do so due to the fact that they wish to make a difference and continue their tradition.

If you donate your body to science, your cremation will certainly be totally free. As cremation can in some cases be costly, this is an exceptional means to reduce prices and still be cremated. Bodies used for scientific research are only made use of for a few weeks, then their ashes are returned to their liked ones.

Funeral Expense Coverage

Think about a final expense plan as a way to attend to a cremation and funeral service. Final expenditure insurance coverage does enable a cash value to develop because it's a form of a whole life insurance coverage plan. The financial savings need to accrue, and there are some things to maintain in mind when you desire to obtain versus the cash worth.

Term life insurance policy plans do not have a cash worth. The money worth develops due to the fact that it runs like an interest-bearing account within the policy. To determine the cash worth, subtract the price of insurance and various other insurance policy costs from the overall amount of premiums paid. With final expense, it feels like you will not have the ability to benefit from it, since its main objective is to pay out a survivor benefit to your liked ones after you pass away.

You can use the cash worth for any type of number of things, yet individuals generally utilize it to pay medical financial obligations or make superior payments. This can be performed in a number of various methods initially, you can give up component of your plan, however that will reduce into your survivor benefit.

This isn't typically a difficult job, but when you pay plans, you're repaying the amount you were lent plus passion. In many cases, the passion rate can be as much as 8%. If you have an outstanding balance by the time you pass away, the amount you owe will certainly be deducted from the survivor benefit.

{kind=link}

Latest Posts

National Seniors Insurance Funeral Plan

Funeral Expense Insurance For Seniors

Final Burial Insurance